At the high-profile FII Miami summit, global investors and policymakers confront a paradox: a region rich in opportunity, yet constrained by the very systems meant to unlock it

In a ballroom overlooking the Atlantic in Miami Beach, the conversation was not about whether Latin America has potential. That question, for this audience, had long been settled.

Instead, the debate at the Future Investment Initiative PRIORITY Summit turned on something far more difficult—and far more consequential:

Why, despite decades of promise and billions in capital, has Latin America struggled to build the infrastructure needed to turn potential into sustained growth?

The session, titled “Enabling Conditions for Long-Term Investment in LATAM: Can Infrastructure Deliver?”gathered investors, policymakers and industry leaders at a moment when global capital is shifting, supply chains are being redrawn, and emerging markets are once again competing for long-term attention.

Latin America, by most measures, should be well positioned. With a combined economic output of roughly $5 trillion, vast reserves of critical minerals, expanding cities and a young population, the region sits at the intersection of some of the most important trends shaping the global economy—from energy transition to food security.

And yet, as speaker after speaker made clear, the central obstacle is neither demand nor capital. It is execution.

A Region Defined by Contradiction

The contradictions are strong.

Nearly one-third of Latin Americans still lack access to basic infrastructure—roads, reliable electricity, water systems—conditions that would be considered foundational in developed economies. At the same time, global investors are actively searching for long-duration, real-economy assets capable of delivering stable returns in an uncertain world.

The mismatch is striking: a region in need of infrastructure, and a global market eager to finance it.

But between those two realities lies a gap—one defined by regulatory complexity, political volatility and a persistent shortage of what investors call “bankable projects.” “Capital is not the issue,” one participant said during the discussion. “Deploying it is.”

That distinction has become a defining theme not only of the Miami summit, but of the broader global investment landscape. In an era of higher interest rates and increased geopolitical risk, capital has not disappeared—but it has become more selective, more disciplined, and less forgiving.

Infrastructure as Destiny

For much of the past two decades, Latin America’s growth story has been tied to commodities—soy, copper, oil, lithium. But the conversation in Miami suggested a shift underway.

Infrastructure, once treated as a secondary concern, is now being reframed as the central determinant of economic destiny.

WTTC Welcomes Manfredi Lefebvre as New Chair at Global Summit Opening Ceremony

Read WTTC’s press release to learn more.

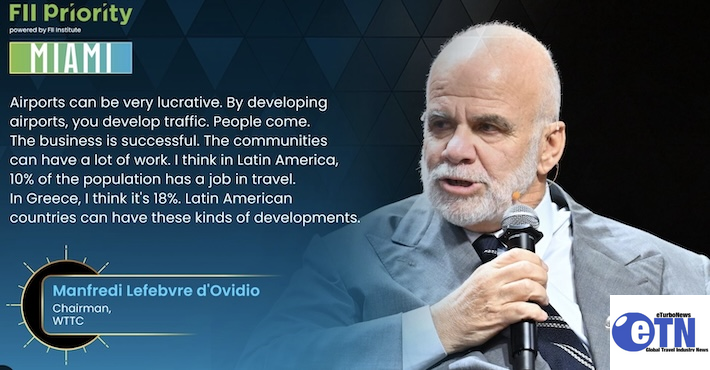

Among the most powerful voices making that case was Manfredi Lefebvre, chairman of the World Travel & Tourism Council, who approached the issue from the perspective of global mobility and tourism. “Infrastructure is not a cost,” he told the audience. “It’s a multiplier.”

Lefebvre is also Executive Chairman of the Monaco based Heritage group, and A&K Group.

The numbers he cited were intended to reframe the debate in stark economic terms: Every dollar invested in infrastructure, he said, can generate as much as four dollars in return.

That multiplier effect, long cited in development economics, takes on new urgency in a region where growth has often been uneven and vulnerable to external shocks.

But Lefebvre’s argument went beyond abstract returns. He pointed to a more immediate and visible consequence of underinvestment: connectivity—or the lack of it.

Manfredi Lefebvre d’Ovidio |

The Geography of Disconnection

Despite its size and population, Latin America accounts for just a small fraction of global air traffic—roughly 5.4 percent, according to figures cited during the session. The implications are both economic and symbolic.

Air connectivity is not simply about tourism; it is a proxy for integration into the global economy. It shapes trade flows, business travel, investment decisions and the movement of ideas.

For European travelers heading to Latin America, Lefebvre noted, many routes still pass through Miami—a reflection of the region’s fragmented aviation networks. “Most of the flights for Europeans which go to Latin America pass through Miami,” he said, underscoring both the importance of the city as a gateway and the limitations of intra-regional infrastructure.

The consequence is a kind of structural under-connection: a region rich in destinations, resources and markets, yet insufficiently linked both internally and externally.

Tourism as a Case Study

If infrastructure is the foundation of economic activity, tourism offers a clear illustration of both its potential and its constraints.

Travel and tourism already account for about 10 percent of Latin America’s GDP, and projections suggest that more than 50 million visitors could arrive annually by 2035. Those figures, on their own, point to a sector poised for expansion.

But growth on that scale depends on systems that extend far beyond hotels and attractions: airports capable of handling increased traffic, roads that connect urban centers to remote destinations, energy systems that can support expanding demand.

Without those systems, demand risks outpacing capacity—a scenario that can stimulate growth as effectively as a lack of demand.

The $150 Billion Question

Estimates presented during the summit suggest that Latin America would need to invest approximately $150 billion annually in infrastructure to close existing gaps and meet future demand.

Current levels fall far short of that target, hovering at about 2.4 percent of GDP. The shortfall represents more than a funding gap; it is a measure of lost opportunity—projects delayed, growth unrealized, competitiveness diminished.

And yet, paradoxically, the scale of the gap also represents an opportunity for investors. In a world where traditional safe assets offer limited returns, infrastructure in emerging markets has become increasingly attractive—provided the risks can be managed.

Public-Private Partnerships: Promise and Limits

One mechanism frequently cited as a solution is the public-private partnership, or PPP—a model designed to combine government oversight with private-sector efficiency and capital.

In Latin America, PPPs have delivered notable successes. Colombia, for example, has developed tens of billions of dollars in transport projects through such partnerships. Brazil and Chile have also attracted international investors through structured infrastructure programs.

These examples demonstrate that, under the right conditions, large-scale projects can be financed and executed.

But they also highlight a key point: success is uneven.

For every functioning PPP, there are projects stalled by legal disputes, regulatory changes or financing challenges. The model, while proven, is not a panacea.

It requires stable policy environments, transparent processes and credible institutions—conditions that vary widely across the region.

Risk, Resilience and the Long View

Another dimension of the discussion centered on resilience—both economic and environmental.

Infrastructure built today will shape the region’s trajectory for decades, particularly as climate risks intensify. Investments in resilient systems—whether flood defenses, energy grids or transport networks—can reduce long-term costs and protect economic stability.

Lefebvre cited estimates suggesting that Well-planned infrastructure could save as much as $9 trillion over the next two decades by mitigating economic and climate-related risks.

Such figures are necessarily broad, but they reflect a growing consensus: resilience is not an optional feature of infrastructure; it is a core requirement.

Policy as the Deciding Factor

If the challenges of infrastructure investment can be summarized in a single word, it may be “confidence.”

Investors are willing to commit capital over long horizons—but only when they have confidence in the rules governing that investment.

That confidence depends on factors that are often outside the control of individual projects:

- Regulatory stability

- Legal clarity

- Predictable taxation

- Transparent procurement processes

Inconsistent or shifting policies can quickly erode that confidence, increasing perceived risk and raising the cost of capital.

Conversely, countries that establish clear and stable frameworks can attract sustained investment—even in complex or capital-intensive sectors.

A Global Context: Capital in Motion

The conversation in Miami did not occur in isolation. It was shaped by broader shifts in the global economy. Capital is moving—not retreating, but reallocating.

Geopolitical tensions, supply chain disruptions and the transition to renewable energy are prompting investors to reconsider where and how they deploy funds.

In this environment, Latin America is increasingly viewed as a strategic destination—one that offers diversification, resource security and growth potential.

But competition is intensifying. Other regions, from Southeast Asia to parts of Africa, are also seeking for the same pools of capital.

To succeed, Latin America must do more than present opportunities; it must deliver them.

From Potential to Performance

For decades, discussions about Latin America’s economic future have been framed in terms of potential. The language of the Miami summit suggested a shift toward something more concrete: performance.

Potential, after all, is not a scarce resource. Many regions possess it. What distinguishes those that succeed is the ability to translate potential into measurable outcomes—completed projects, functioning systems, sustained growth.

That translation depends on execution.

And execution, in turn, depends on a combination of factors that extends beyond any single investment:

- Institutional capacity

- Political wants

- Technical expertise

- Cross-border collaboration

The Human Dimension

Behind the statistics and investment models lies a more immediate reality. Infrastructure is not an abstract concept; it is the network of systems that shape daily life—how people move, work, access services and connect to opportunity.

For the roughly 30 percent of Latin Americans who lack basic infrastructure, the stakes are measured not in GDP points or return ratios, but in access—to jobs, education, healthcare.

Closing that gap is as much a social imperative as it is an economic one.

A narrow window

The sense emerging from the Miami session was not one of pessimism, but of urgency.

Latin America, participants suggested, may be entering a window of opportunity—one defined by favorable global conditions, investor interest and shifting economic dynamics.

But windows, by their nature, do not remain open indefinitely. If the region can address its structural challenges—if it can build the regulatory frameworks, develop bankable projects and execute at scale—it may attract the sustained investment needed to transform its infrastructure landscape.

If not, capital will move elsewhere.

The Question That Remains

As the session drew to a close, the central question remained unresolved, but more clearly defined:

- Not whether Latin America should invest in infrastructure.

- Not whether capital is available.

- But whether the region can create the conditions necessary to turn investment into reality.

In the words echoed throughout the discussion, and reinforced by Manfredi Lefebvre’s intervention: